What Does Volatility in the Equity Markets Mean for Investors?

What’s happened year to date?

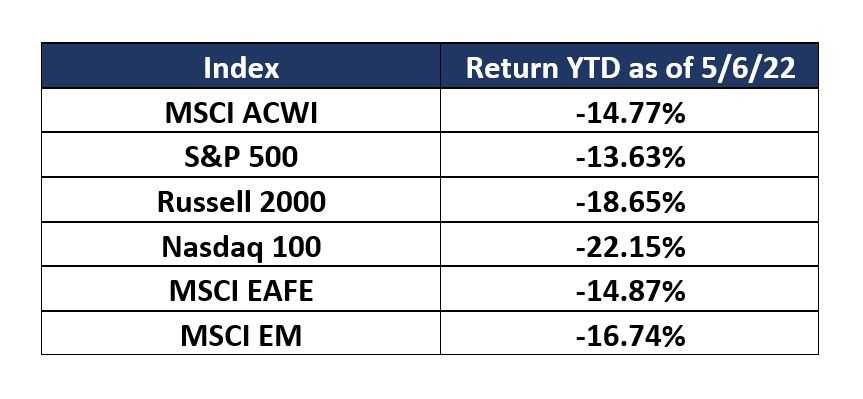

Despite lingering supply chain issues and growing inflation concerns, investors saw strong equity performance in 2021, both domestically and internationally, as the S&P 500 and MSCI ACWI returned 28.7% and 19.0%, respectively. In contrast, investors have experienced significant volatility and market selloffs in 2022 that have negated most, if not all, of last year’s gains. As of May 6, 2022, the Year-To-Date benchmark returns are as follows.

Why?

With slowing global growth, increased volatility in equity markets was not entirely unexpected, but there are several primary contributing factors to highlight.

Inflation – Due to the COVID-19 pandemic, Americans received unprecedented fiscal and monetary stimulus in 2020. At the same time, travel restrictions and supply chain issues allowed consumers to start saving more. As the economy and the world started to reopen in 2021 “revenge spending” took over. This pent-up demand was met with limited supply and consumer price inflation (as measured by Consumer Price Index or CPI) accelerated from 2.6% year-over-year in March 2021 to 8.5% year-over-year in March 2022—the highest since the 1980s. Excessive inflation hurts consumers due to increasing prices, which weighs on the economy.

Rising Interest rates – To combat inflation, the Federal Reserve (Fed) has signaled that it will raise interest rates until the Fed funds rate reaches 3-3.25%. Rising interest rates increase the cost of borrowing, which is a headwind for future economic growth, and raise corporations’ cost to finance capital improvement projects. Mortgage rates also tend to rise, evidenced by the 30-year fixed rate recently hitting 5.27%, the highest since 2009. Rising interest rates also tend to lower stock valuations, which is what investors have witnessed this year.

The Russia/Ukraine War – To the world’s surprise and dismay, Russia invaded Ukraine on February 24, 2022. Sanctions were imposed on Russia that have significantly impacted their economy, but Russia is proving resilient and unwilling to abandon the war. Russia and Ukraine are some of the world’s top exporters of wheat, metals, fertilizers, and especially oil and gas. Therefore, this war is a primary contributor to the soaring commodity and energy prices. Rising commodity prices increase raw materials costs for businesses, which either lowers profits or is passed along to consumers through higher prices. In addition to the pressure on commodities, the uncertainty of how long the war will last and who else might get involved is adding to the volatility.

How do these circumstances compare historically?

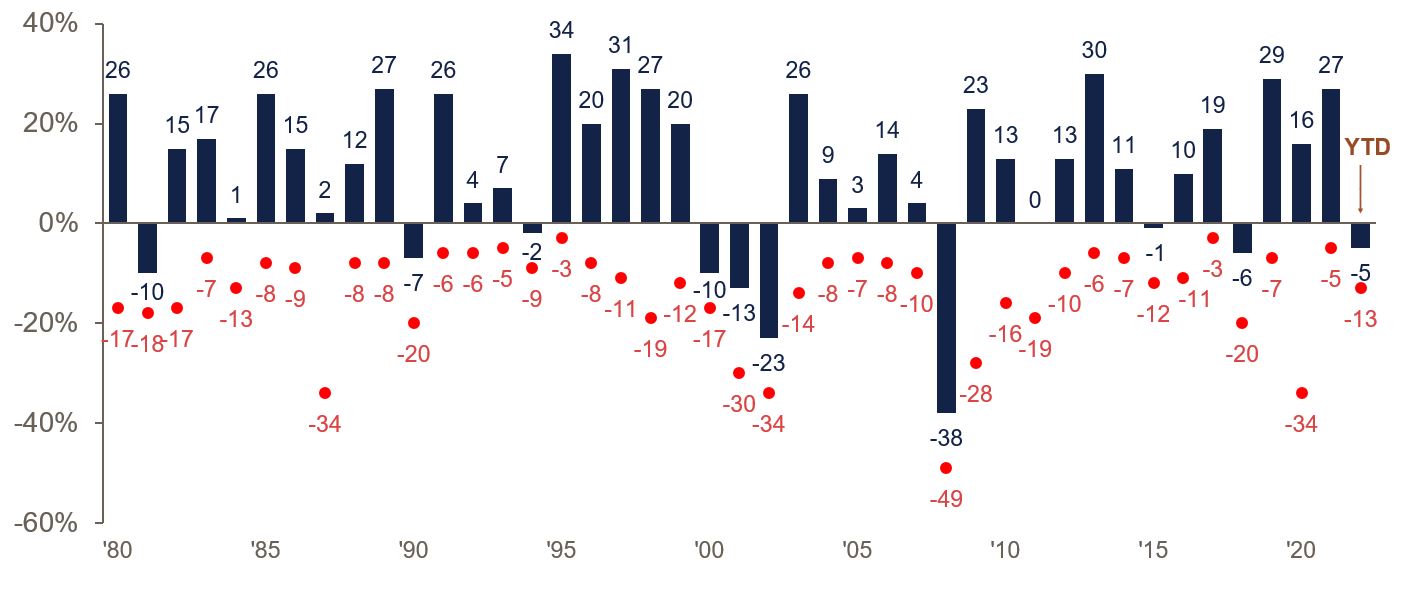

These series of events—combined with a reopening economy after a global pandemic—have never happened simultaneously before, but the world has seen numerous wars and geopolitical events throughout history. To put the current circumstances in perspective based on the S&P 500, the average drawdown of the 12 worst recessions is -36%. The current drawdown is approximately -13%, which is closer to a typical drawdown in any given year, which is -14%.

Despite average intra-year drops of 14.0%, annual returns are positive in 32 of 42 years.

U.S. Stock Market Calendar Year Returns vs. Max Drawdowns

Source: Standard & Poor’s, FactSet, J.P. Morgan Asset Management; U.S. Stock Market = S&P 500. Returns are based on price index only and do not include dividends. Max Drawdown refers to the largest market drops from peak to trough during the year and is represented by a red dot and red (negative) return. Returns shown are calendar year returns from 1980 to 2021, year to date is as of 3/31/22. Past performance does not indicate future results.

How should investors navigate this volatility?

Stay invested – After the 12 worst drawdowns in stock market history, the market ended positive one year later in all instances except 1933, and the probability of experiencing positive equity returns increases significantly if investors stay in the market longer than five years. Stocks are a long-term asset. Historically, short-term volatility has little impact on long-term returns.

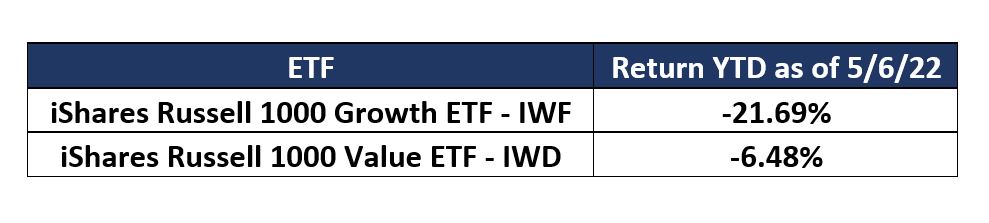

Look for value to outperform growth in a rising interest rate environment – Growth stocks typically promise high sales and market share growth with a higher future return of capital in exchange for low or no profits today. Interest rates are used in the valuation of stocks, and higher interest rates lead to lower discounted present values, especially in growth stocks. When interest rates were near 0%, investors could take more risk and invest in speculative growth stocks. In this new interest rate environment investors are de-risking and investing in higher-quality, value stocks, which is evident by looking at the Russell 1000 Growth and Value ETFs.

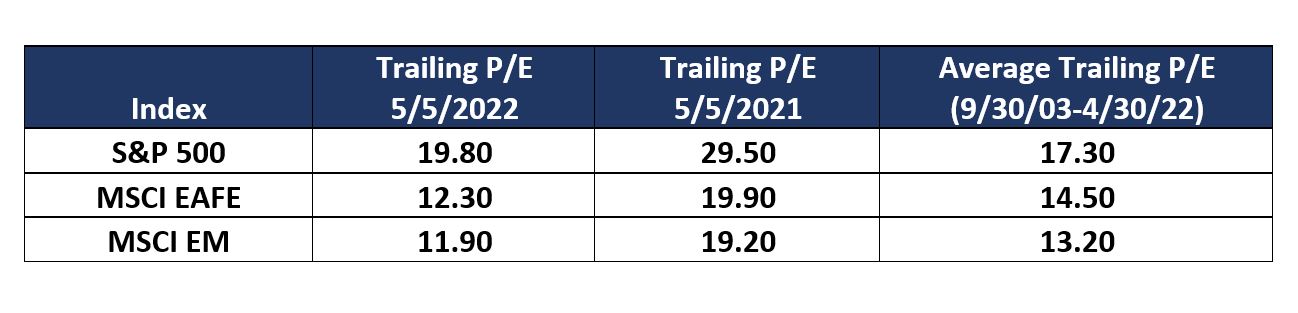

Consider investing in equities – While still elevated, equity valuations, as demonstrated by trailing Price-to-Earnings (P/E), have fallen back within 20-year historical ranges. For investors with excess liquidity, this might present an opportunity to reinvest. Keep in mind though that valuations remain elevated compared to the last 100 years and could continue to fall given expected lower economic growth.

At Blue Trust, we believe in the principles of uncertainty and instability. It appears the world is bracing for a potential recession, but the economy is currently supported by strong consumers (who still have high levels of savings and abundant job opportunities) and vibrant corporations that are not overly indebted and are still enjoying high earnings. The war, inflation, and rising interest rates will almost certainly bring more fear and volatility, but no one knows what the future holds so we encourage our clients to diversify and stay invested over the long term to help meet their financial goals.

14970415-05-22